Currently retirement readiness depends heavily on the State Pension as people are not making adequate private pension provision. Only 29% of us know what we need to live on in retirement.* It is projected that the State Pension will become unsustainable in its current form due to demographics.** To combat the aging population, the State have tightened eligibility conditions and the age payable is rising.

Irish Life EMPOWER aims to achieve better outcomes at retirement for members so that they will have an adequate pension whether the State Pension is available or not. This article will discuss how Irish Life EMPOWER can benefit employees when it comes to saving for their retirement.

Technology and communications

The ways in which we now communicate have been transformed by technology. Google, Facebook, Twitter, Instagram, Snapchat, have changed the way we communicate.

And why have they been so successful? Because they all have a common approach that we now use in Irish Life’s EMPOWER communications:

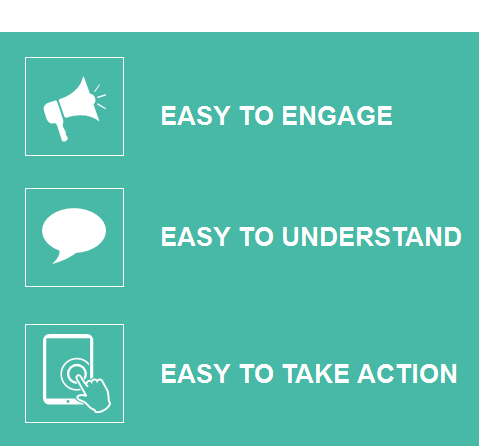

Easy to engage

Making it easy to engage is crucial to our member communication strategy. Irish Life’s approach uses the best of all modern technologies, including: Apps for smart phones/iPads as well as powerful online content. It’s not just about technology; we use the same approach when meeting people face to face. The key is making it simpler for people to engage with their pensions.

Easy to understand

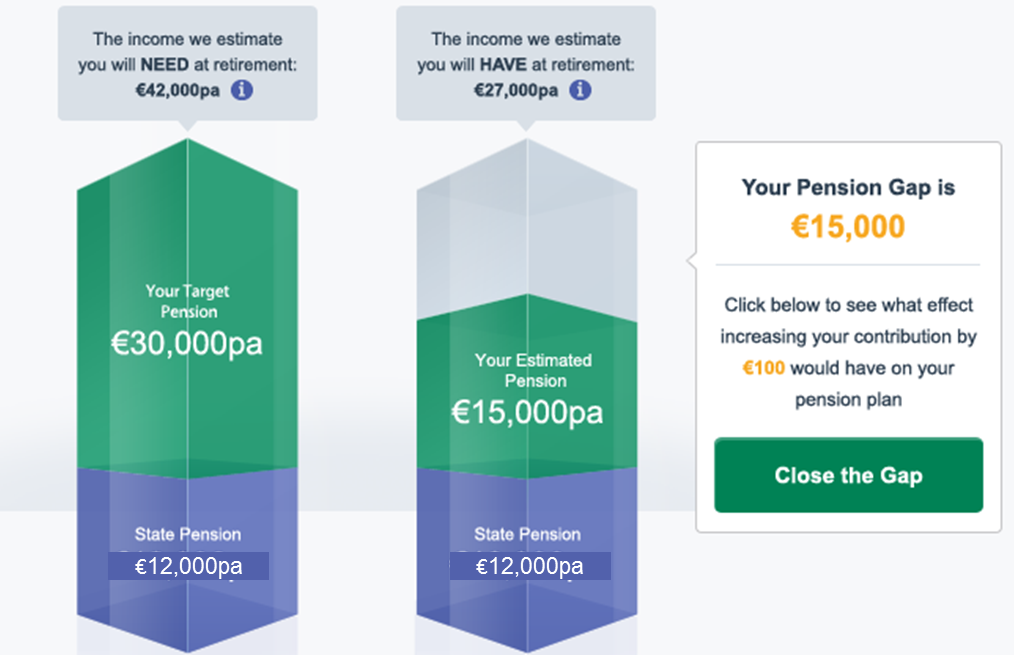

Here’s a visual from one of our employee pension tools.

On the left the member can see their target for retirement, on the right the member can see their likely retirement income. And they can see the difference; we call this the ‘Pension Gap'. Every person using our technology will have a personalised target based on their own circumstances.

This tool is interactive, encouraging members to see:

• What happens if they increase their contributions by 1% p.a., or by €100 a week?

• What happens if they do or don’t have access to the State Pension?

• What happens if they want to retire early or to postpone their retirement?

The simple theme here is to help people to understand how to reduce their "pension gap".

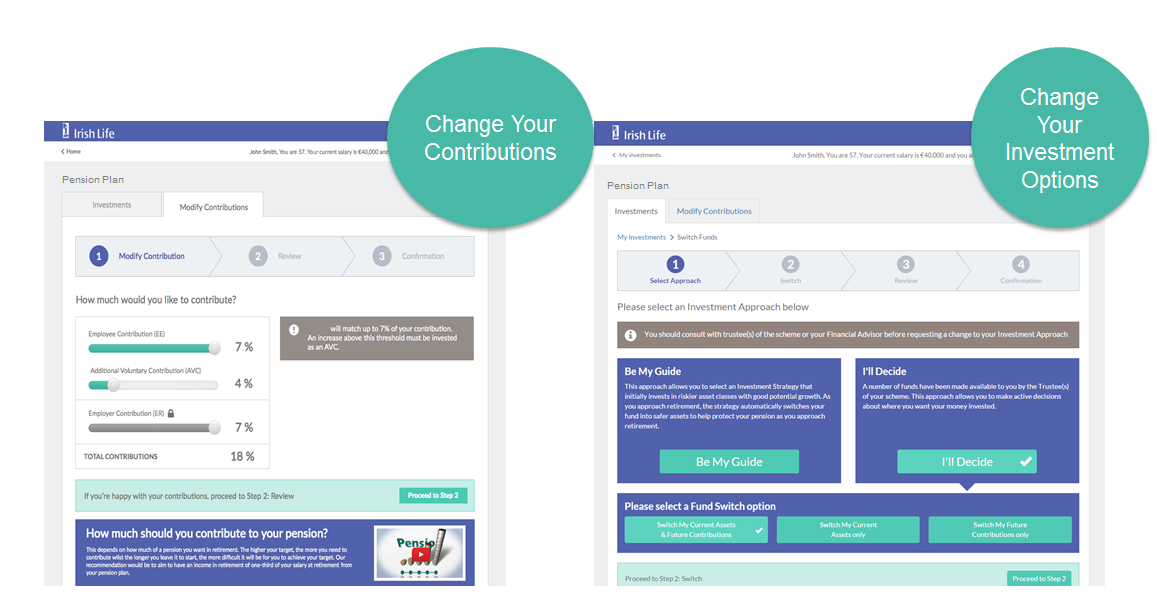

Easy to take action

After they have interacted with this simple tool, we want them to be able to make the change there and then. This technology lets people make their changes online as part of this interactive process. We have taken the hassle out of it. Whether it’s requesting an online fund switch, increasing contributions or paying Additional Voluntary Contributions (AVCs), employees can simply make the change online and our technology takes care of the rest.

Case study

Save more tomorrow

An employer that Irish Life worked with for a long time was in a position to pay salary increases over the next few years. We agreed that it was a good time to re-introduce the pension’s agenda to their work-force.

‘Save more tomorrow’ is one of the easiest ways for employees to promise to do something positive in the future that won’t impact them immediately.

Irish Life built a solution specifically for the client that allowed their employees commit a part of their future salary increases to be paid to better fund their retirement savings. For example, where an employee might be getting a 2% salary increase, the employee would commit to save 1% of this into their pension.

To help employees in their decision making process Irish Life demonstrated the benefits in terms of increased retirement savings, the cost of foregoing some future salary increases and most importantly we made it easy for them to implement their decision. This information was made available online as well as through the member engagement team for face to face meetings.

This resulted in 54% of members opting for the automatic increases.*

This is just one example of how we worked with a client to support their pension agenda with their staff. It’s our job to work with you to come up with the most appropriate solution that will suit you and your employees. Contact your Pension Consultant to find out how we can help you.

Personal Lifestyle Strategy (PLS)

PLS builds on the same EMPOWER principles to help members achieve better results at retirement. The Personal Lifestyle Strategy has helped to remove the investment question that has consumed so much time for trustees and members in the past.

The Personal Lifestyle Strategy offers a truly personal strategy that will:

• Treat each member as an individual – not an average or most common but a truly personalised approach.

• Calculate the best tax free lump sum option for each member based on their individual circumstances.Then it calculates what other retirement options are available as the rules around this can be quite confusing.

• Make sure that each member’s savings at retirement are invested in the most suitable funds to maximise their pension benefits.

• Determine the most appropriate investment options to switch members into as they approach retirement, it takes account each members details such as salary, age,other pension benefits, contribution rates and if they are paying AVCs.

• Automatically switch each member's funds from growth funds to lower risk funds as they get closer to retirement.

Where as other strategies will switch members into a split of bonds, cash and other assets that has no correlation with their needs and such approaches are outdated and are no longer the best options for members.

The Personal Lifestyle Strategy provides a huge benefit to those saving for their retirement. It has become the investment vehicle of choice for trustees and members that we work with.

Please contact your Pension Consultant for more information on how Irish Life can help provide better outcomes at retirement for your employees.

*Source: Irish Life Corporate Business, 2015.

**Source: Society of Actuaries Ireland & PublicPolicy research report carrued out by Milliman, 2015.