Sovereign Annuities

Sovereign annuities are a product (certified by the Pensions Authority) available to trustees of occupational pension schemes. Irish Life’s sovereign annuity product* was certified by the Pensions Authority in December 2012.

Sovereign annuities are cheaper than traditional annuities because they invest in bonds (Irish Amortising Bonds) issued by the National Treasury Management Agency (NTMA).

These bonds offer higher returns than those available, for example, on German and French bonds which are typically used for pricing of traditional annuities. Although the yields available on Irish Government bonds have fallen dramatically since the height of the financial crisis (reflecting much improved market sentiment towards Ireland) there are still significant savings on sovereign annuities against conventional annuity products.

In April 2013 the discount was around 15% but this has reduced since the Irish spread over lowest risk has reduced and now typically varies between 1% and 5% (but depends on scheme profile and yields on any day). The discount arises as unlike conventional annuities, Irish Life has the right to reduce or cease annuity amounts if payments are not received on the bonds as expected, termed a “non-performance event”.

*Pensions Authority reference SA(IL)01

Use of Sovereign Annuities – Defined Benefit Wind Ups

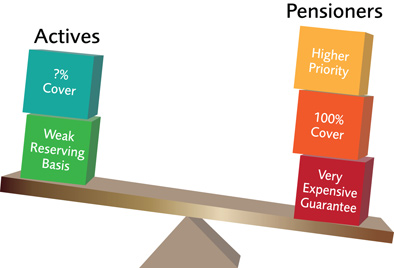

When a Defined Benefit pension scheme winds up the pension scheme’s entire assets are distributed to the members (if there isn’t a surplus in the pension scheme). The Trustees are responsible for deciding on a fair distribution between the different categories of members. After allowing for Additional Voluntary Contributions and expenses, traditionally the first use of the scheme assets was to secure conventional annuities for retired members. The balance of the fund was available for distribution to active and deferred members.

In an adequately funded pension scheme (i.e. one that meets the Minimum Funding Standard) this is a reasonable arrangement. However, many pension schemes do not meet the Minimum Funding Standard. As pensioners are a higher priority in the statutory windup rules they are still entitled to their full benefit. This means that after buying the pensions using conventional annuities the remaining assets are inadequate to fully provide for the liabilities for active and deferred members.

In these circumstances sovereign annuities are a very useful option for Trustees because they may:

- Make a saving on the cost of securing pensions for retired members

- Ensure retired members continue to get their full pension – except in the event of a non-performance event down the road.

- Tip the scales more in the favour of active and deferred members – who are only entitled to whatever is remaining after the pensions have been bought out.

Buying sovereign annuities provides pensioners with their pensions and allows for more assets to be used to secure benefits for active and deferred members. Trustees will need good reasons to justify this. These include:

- Active and deferred members may not be getting anywhere near 100% of their minimum transfer value.

- Even getting their full minimum transfer value active and deferred members are unlikely to get the pension they have accrued as the assumptions behind this calculation are optimistic – 7% investment returns and a 30% discount on current annuity costs.

- Purchasing sovereign annuities leaves both retired and active and deferred members with some risk – the former are exposed to non-performance risk, the latter are exposed to investment and annuity rate risk.

Sovereign Annuities in more detail

Sovereign annuities pay a pension for life. However in the event of a non-performance Irish Life will reduce the pension payable (possibly to zero) in line with the rules in the annuity policy. A non-performance event is a sovereign bond default or a sovereign bond restructuring. The Irish Life products works on a “cash flow basis”. This means that any default on the NTMA bonds is reflected in a direct reduction (or stoppage) of the pension.

A number of trustees have brought in a risk control measure and bought a conventional annuity underpin. One example involves the trustees buying a certain amount (say €5,000 per annum) of standard annuity (which does not depend upon bond performance) and using the sovereign annuity as a top up for higher pensions.

This reduces the financial saving, of course, but brings greater investment certainty.

Sovereign annuities are a useful new option for trustee consideration when addressing pension fund deficits. However, they also bring new risks for pension schemes and their members that need understanding. Trustees should weigh up pros and cons carefully. As ever, it is very important for them to get full actuarial, legal and investment advice before making any decisions.

If you would like more information on the our sovereign annuity product please contact your account manager or our Annuity Product Manager - Shane O’Farrell (7042869 or shane.ofarrell@irishlife.ie).

Warning: The income that you get from this product may be reduced in payment or even cease.