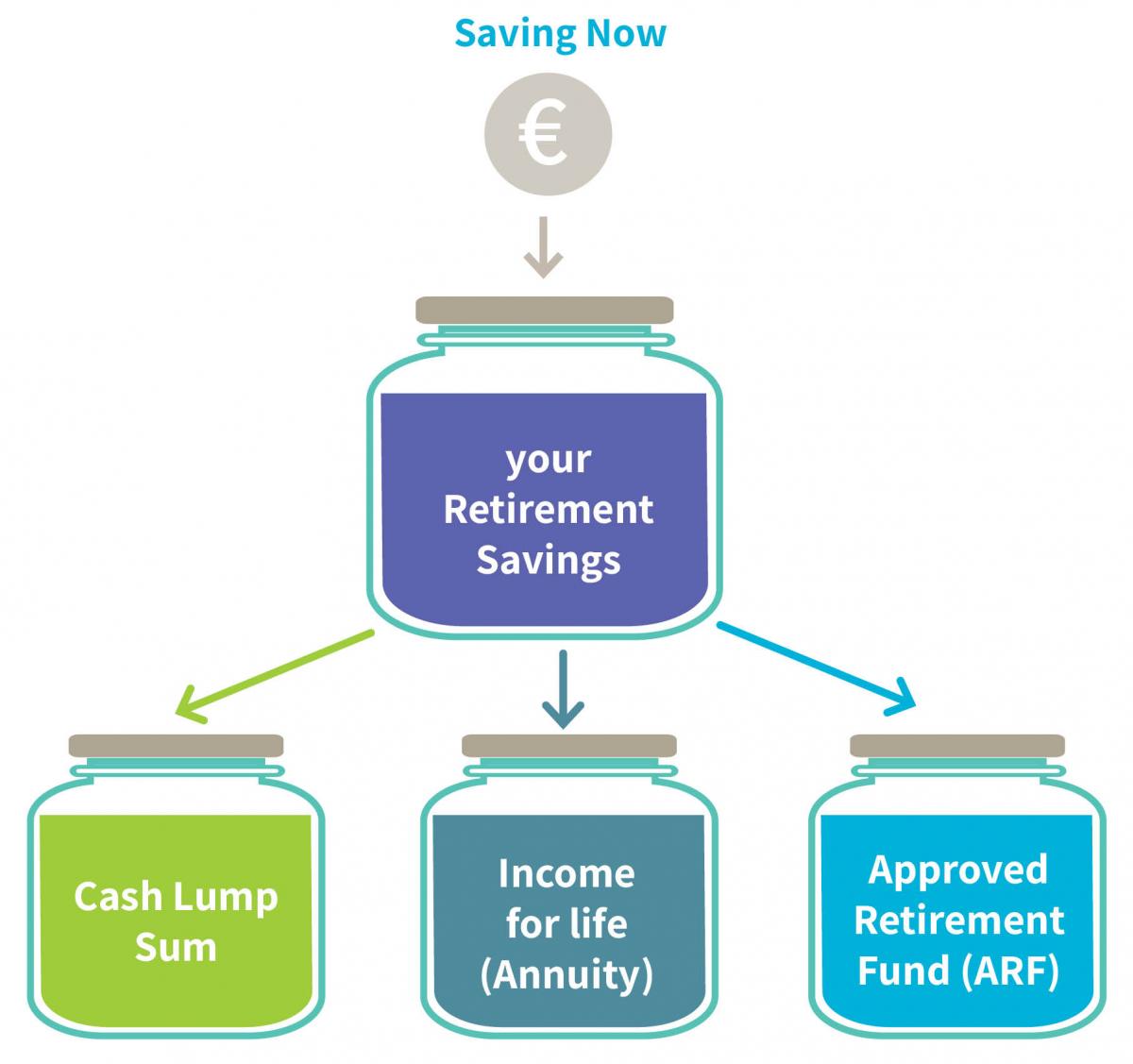

Are you over 50, have left your previous employer and would like to claim your pension benefits?Deciding how to use your retirement pot is one of the biggest financial decisions you will make with consequences for the rest of your life. We strongly advise that you seek independent financial advice and speak to a financial adviser or broker. If you do not have one, you can arrange to speak to an Irish Life financial advisor by clicking here. Let’s look at the options available:

|

||||||||

|

||||||||

|

*Please see the next page for the tax treatments on these lump sums. **These amounts may change (up or down) as specified by the Government. The amounts quoted are correct as at December 2022. |

||||||||

|

|

||||||||

|

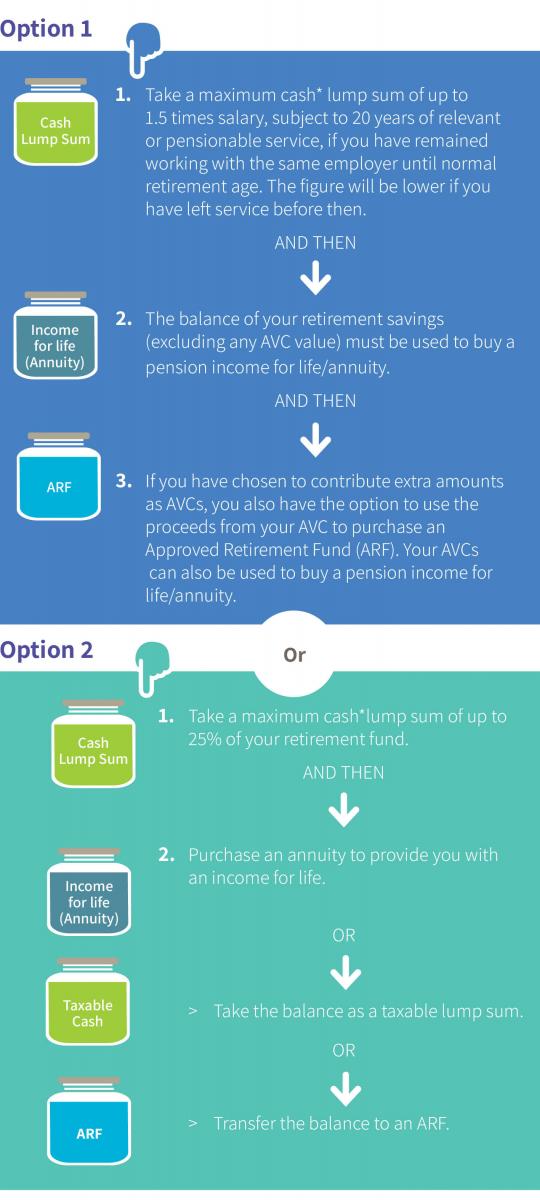

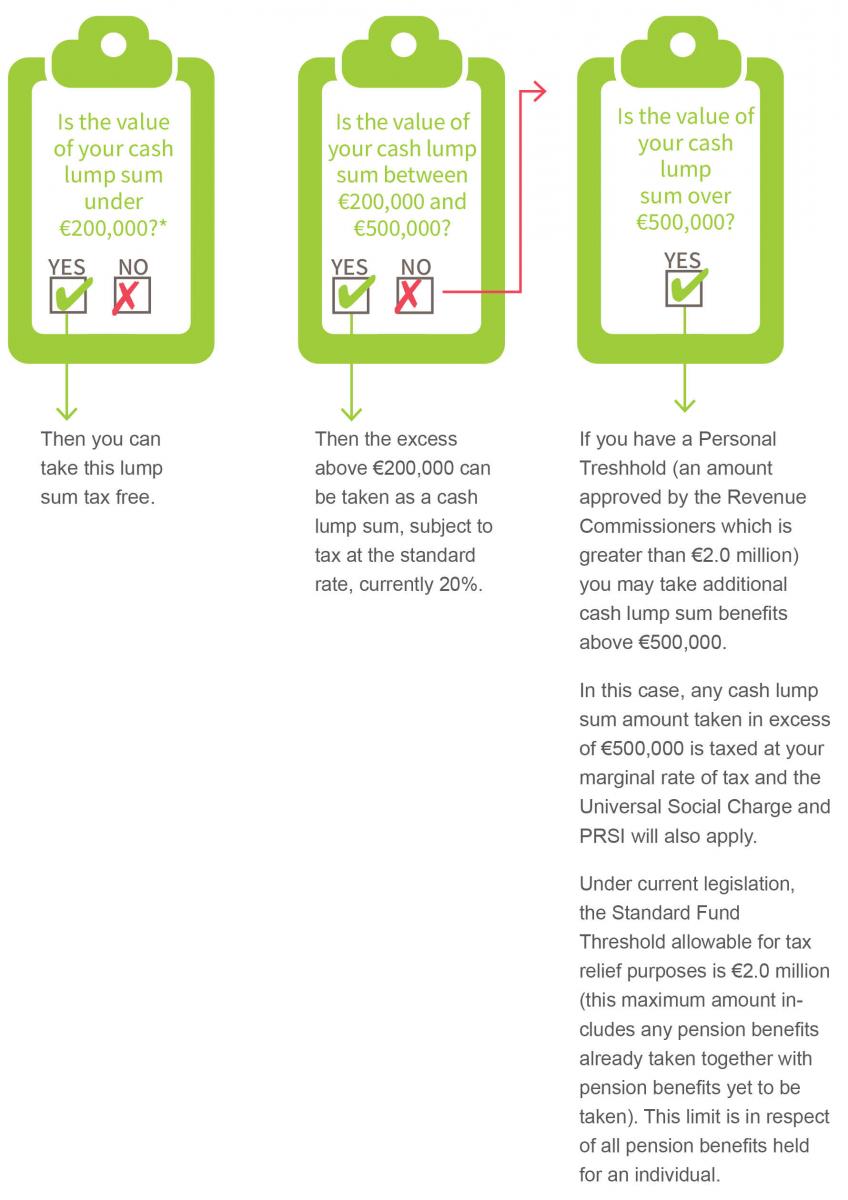

The cash lump sum is a cash amount you can access depending on the value of your pension pot. Under option 1 above, the cash lump sum amount will also depend on your salary, your length of service with your employer and whether you are retiring at normal retirement age or are early retiring. Under option 2, the tax-free lump sum will be based on 25% of your retirement fund at the point of retirement. In certain circumstances, it may also be possible to take a taxable payment for the remainder of the pension value, subject to certain Revenue restrictions. This payment will be subject to Income Tax, the Universal Social Charge and PRSI, if applicable. An administration fee of €36 will also apply. There are other tax rules which apply to the Cash Lump Sum. The first €200,000 is tax free, the next €300,000 will be taxed at the standard rate of income tax with any amount over €500,000 being taxed at your marginal rate of income tax. Any tax-free retirement lump sums taken on or after 7 December 2005 will count towards the above limits. You should tell us if you have previously received a tax-free lump sum from any other pension(s) by completing the Other Pension Benefits form. |

||||||||

|

1. Tax-free cash lump sum: €85,000 |

||||||||

|

Jane has a pension pot size of €340,000 and under the Revenue rules and her service with her employer (40 years of service), Jane could take a tax-free lump sum, at normal retirement age) of either: |

||||||||

150% of €60,000 = €90,000 or |

25% of €340,000 = €85,000 |

|||||||

|

Remember that the lifetime limit for tax free cash from all pension schemes is €200,000 so Jane was able to take this €90,000(X) tax-tree as she had not previously taken a lump sum from a pension scheme. Jane decided she wanted flexibility over how she could access her retirement savings fund and chose the ARF option. instead of the annuity option. Having chosen the ARF option. Jane could take only €85,000 (25% of her pension pot) as a cash lump sum. Please note that Revenue has strict guidelines around the amount of tax free lump sum that can be taken – the amount may be lower than advised if you retire before normal retirement age, and may also depend on your length of service with the employer. |

||||||||

|

Tax treatment of your Cash Lump Sum |

||||||||

|

||||||||

*Tax free lump sums taken on or after 7 December 2005 will count towards using up the tax free amount. So if you have already taken tax free cash totalling €200,000 or more since December 2005, any further retirement lump sums paid to you will be taxable. *Tax free lump sums taken on or after 7 December 2005 will count towards using up the tax free amount. So if you have already taken tax free cash totalling €200,000 or more since December 2005, any further retirement lump sums paid to you will be taxable. |

||||||||

|

You will find specific information in relation to the maximum value you can draw down in the form of a cash lump sum in your Leaving Services Options letter. You will receive this letter in the post within 2 months of retiring. |

||||||||

|

Income for life (Annuity) |

||||||||

|

You have the option to use your full fund, or any balance remaining after taking a tax-free lump sum, to purchase an income for life also known as an annuity. An annuity suits those who have a low appetite for risk and demand certainty of income in retirement. The amount payable will depend on the value of your pension plan and your age/life expectancy. You can choose to add various options to your annuity such as: |

||||||||

|

||||||||

|

Guarantee option |

||||||||

|

This option allows the annuity to continue to be paid for the remainder of the guaranteed period in the event of your death. You can select a guarantee period of 5 or 10 years. |

||||||||

|

Annual increases |

||||||||

|

You decide how you would like to take your pension payments and can choose to take a lesser amount at the start and increase this into the future or increase your payments in line with inflation. Below are examples of pension plan options available to you: |

||||||||

|

||||||||

|

Dependent/Spouse Benefit |

||||||||

|

You may use part of your pension to purchase a pension for a dependent or spouse. The person nominated must either be a spouse or financially dependent on you. This pension then becomes payable upon your death or at the end of the guarantee period of your own pension, if later. The amount payable can be chosen by you; for example, you may opt to have 50% or 100% of your pension paid to your spouse or dependent following your death. |

||||||||

|

Approved Retirement Fund (ARF) |

||||||||

|

An ARF is a special investment fund which can give you increased flexibility in terms of how you use your pension fund after retirement. With an ARF you manage and control your pension fund. You can be happy in the knowledge that you can withdraw as much of this as you wish, should you ever need to. Any withdrawals you take from your ARF will be subject to income tax*, the Universal Social Charge and PRSI (if applicable). In the meantime, the fund will continue to be invested in funds of your choice. By investing in an ARF, your money can remain invested in funds that can both grow and fall. You can choose to invest in an ARF now and then take out an annuity at a later stage. The option to invest in an ARF will depend on the tax-free lump sum option you have chosen. If you have chosen option 1 (as described above), the balance of your employee and employer contributions must be used to purchase an annuity. If however you have paid Additional Voluntary contributions, then you could invest these contributions into an ARF. Under option 2, the balance remaining after you have received your tax-free lump sum (i.e. up to 25% of your retirement pot) can be fully invested into an ARF, should you choose to do so. |

||||||||

|

Documents required |

||||||||

|

Please return the following documents via email to happytohelp@irishlife.ie and remember to quote your member number in the subject line. We will not be able to process your application without the below information: 1. Option Election Form signed by you and your spouse (if applicable) 2. Other Pensions Benefits Form 3. Trustee Authorisation* 4. Passport/Driver’s Licence for you and your dependent/spouse (if applicable)** 5. Bank Statement*** 6. Marriage Certificate (if choosing a dependent/spouse pension) 7. Willing and able confirmation (if transferring to an ARF)**** *We will arrange Trustee Authorisation on your behalf. Please leave the information in relation to this blank on the Options Election form. **The image on the passport or driver’s licence must be visible. You can either scan a copy or send a picture from your phone. ***Your bank statement must be for the account into which the funds will be paid. It must include first-name, surname, address details, IBAN and be less than 6 months old. ****The Willing and able letter/email confirms the new provider has set up the ARF. You need to contact the new provider and request they email a ‘Willing and able’ confirmation. They should then email this to happytohelp@irishlife.ie quoting your member number which includes the new providers Bank, IBAN and BIC details. Once you have completed and returned all the above documentation, we will then request Trustee authorisation and, once received, process your claim request within 5 working days. We will confirm payment via post with the funds arriving to your account within 3-4 working days. |

||||||||

Irish Life Health

Welcome to Ireland’s newest health Insurer, Irish Life Health. Bringing fresh options and innovation to the health insurance market.

Irish Life

Irish Life the largest life and pensions group and fund manager in Ireland, employing 2,000 people and servicing one million customers.

Irish Life Investment Managers

Managing assets in excess 39bn, ILIM manages money on behalf of multinational corporations, charities and domestics.